MARY E. POWELL, September, 2019

![]()

In the last few months, the Internal Revenue Service (IRS) and the U.S. Department of Health and Human Services (HHS) have issued rules that impact the cost that group health plans (GHPs) can charge participants for certain prescription drugs. This article explains those rules and also takes a critical look at how those rules actually impact GHPs and participants.

List of Preventive Care Services and Drugs — Expanded?

In July of 2019, the IRS issued Notice 2019-45 (the “Notice”), which expanded the list of preventive care benefits that may be provided by a high deductible health plan (HDHP) prior to the deductible being met without running afoul of the Health Saving Accounts (HSA) rules.

Background

The basic rule under Internal Revenue Code (the “Code”) § 223 is that individuals who are covered by an HDHP generally may establish and make contributions to an HSA (including pre-tax contributions via a Code §125 cafeteria plan) as long as they have no disqualifying health coverage. For the HSA rules, an HDHP must satisfy certain requirements, including that the plan cannot pay for covered benefits — other than preventive care — before participants have met the minimum annual deductible. Until the minimum annual deductible is met, the participants in that HDHP must pay the full cost of medications and services. An HDHP can waive the deductible for preventive care and not have that cause the participant to be HSA-ineligible.

Definition of Preventive Care

For the HSA/HDHP rules, there is no definition in the Code for what constitutes “preventive care.” The IRS provided a safe harbor definition of “preventive care” in IRS Notice 2004-23 which states that preventive care for purposes of Code § 223 includes, but is not limited to, the following: (1) periodic health evaluations, including tests and diagnostic procedures ordered in connection with routine examinations, such as annual physicals, (2) routine prenatal and well-child care, (3) child and adult immunizations, (4) tobacco cessation programs, (5) obesity weight-loss programs, and (6) screening services. IRS Notice 2004-23 states that preventive care does not generally include any service or benefit intended to treat an existing illness, injury, or condition. The IRS has also interpreted the Code § 223 definition of preventive care to include any preventive health services within the meaning of the Affordable Care Act (ACA) market reform rules (IRS Notice 2013-57).

With regard to prescription drugs, IRS Notice 2004-50 states:

Solely for this purpose, drugs or medications are preventive care when taken by a person who has developed risk factors for a disease that has not yet manifested itself or not yet become clinically apparent (i.e., asymptomatic), or to prevent the reoccurrence of a disease from which a person has recovered. For example, the treatment of high cholesterol with cholesterol-lowering medications (e.g., statins) to prevent heart disease or the treatment of recovered heart attack or stroke victims with Angiotensin-converting Enzyme (ACE) inhibitors to prevent a reoccurrence, constitute preventive care.… However, the preventive care safe harbor…does not include any service or benefit intended to treat an existing illness, injury, or condition, including drugs or medications used to treat an existing illness, injury or condition.

How the Previous Guidance Was Implemented

Pharmacy Benefit Managers (PBMs) usually create (and control) the formulary that is adopted by the GHP and that formulary is often driven by the amount of rebates and other indirect compensation that the PBMs will receive. The PBMs also usually create (and control) which drugs will be considered “preventive care” and provided at no cost to participants. Some PBMs take the position that for individuals who have chronic conditions like diabetes, asthma or heart disease, the treatment of those conditions through prescription drugs should be considered “preventive care” because those drugs prevent the occurrence of an additional disease or death. The lists of “preventive care” drugs are different for the different PBMs — depending on how aggressive that PBM is in determining what could be considered “preventive care” for the HSA/HDHP rules.

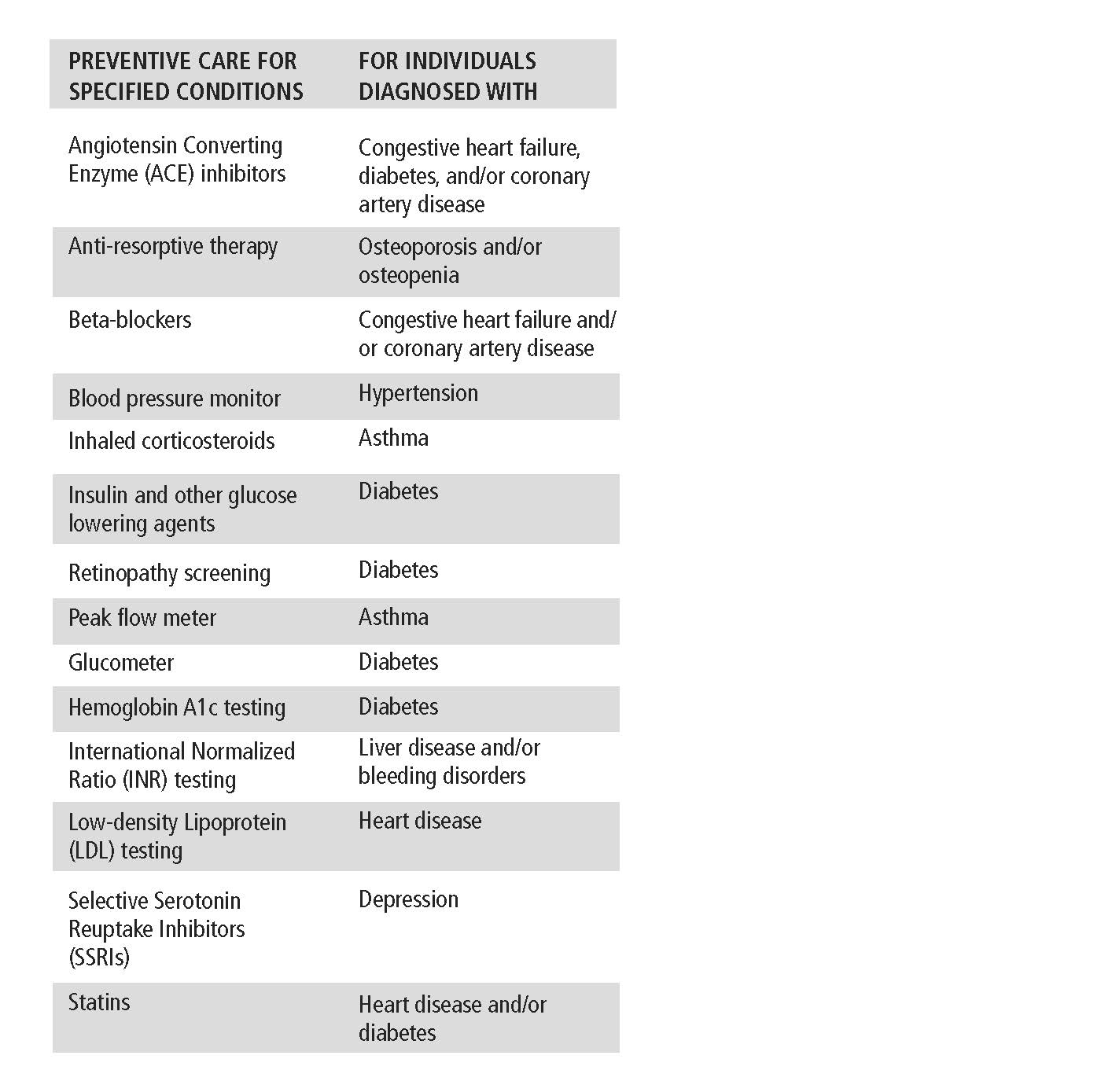

The Change Under the New Notice

The Notice states that the IRS, in consultation with HHS, determined that only certain medical care services received and items purchased, including prescription drugs, for certain chronic conditions should be classified as preventive care for someone with that chronic condition. The Notice provides a specific list and states, “These medical services and items are limited to the specific medical care services or items listed” in the appendix attached to the Notice. The appendix contains the following chart that lists services and items for individuals with the specified chronic conditions that can be treated as preventive care by HSA/HDHPs:

Potential Impact

With the rise of HDHPs, participants have become acutely aware of the cost of prescription drugs — and the continual increase in costs. Before HDHPs, many GHPs only had a co-pay (such as $15 or $20) for covered prescription drugs, so the true costs of prescription drugs were hidden from participants. HDHP participants pay 100% of costs until the deductible is met, which unmasks the cost of prescription drugs and adds to the public debate about it. However, over the last several years, through the PBM controlled formularies, the costs of many prescription drugs were once again hidden from participants because they were categorized as “preventive care” and provided at no cost to participants. IRS Notice 2019-45 will change that practice.

Many GHPs will adopt the list issued in the Notice. This may be a needed gift for some participants who participated in GHPs that had limited drugs listed as preventive care for someone with a chronic condition. However, for other GHPs, the list of preventive care drugs may be narrowed to take into account the guidance in the Notice.

New Guidance Regarding Coupons Issued by Pharmaceutical Companies and How They Affect HSA/HDHPs

For certain high-cost drugs, pharmaceutical companies will provide individuals with a “coupon” that can be used to assist with the payment for the prescription drug. Participants who were still in the GHP deductible would use these coupons to purchase drugs, but that coupon amount was also being credited against the GHP’s deductible. For example, a participant would be prescribed a brand drug that costs $500. He would go to the pharmacy and pay $100 and use a coupon (paid for by the pharmaceutical company) for the other $400. However, for the purpose of the GHP deductible, the participant would be credited as if he paid the full $500. In response to this, PBMs created a copay accumulator program which was adopted by some GHPs. Copay accumulator programs exclude copay assistance (such as the coupon) from counting toward an individual’s deductible or out-of-pocket maximum. To date, there was very little guidance on these programs other than IRS Notice 2004-50, which clarified that the use of a discount card that is available to the general public will not cause a person to become HSA-ineligible.

That changed when HHS issued the 2020 HHS Notice of Benefit and Payment Parameters (“2020 NBPP”), which established different rules regarding when a GHP was required to count the coupons toward the out-of-pocket maximum. However, the guidance in 2020 NBPP with regard to coupons has been put on hold, as described below.

Background

Public Health Service Act (PHSA) § 2707(b), as added by the ACA, provides that a GHP shall ensure that any annual cost-sharing imposed under the plan does not exceed the limitations provided for under § 1302(c)(1) of the ACA (which limits out-of-pocket maximums — OOPMs). In an FAQ, the three applicable Departments (Treasury, Department of Labor and HHS) stated that they read PHSA § 2707(b) as requiring all non-grandfathered group health plans to comply with this OOPM rule. HHS has issued regulations under § 1302(c)(1) of the ACA-45 C.F.R. § 156.130 and self-funded GHPs have generally followed those rules for determining the parameters of the OOPM rule.

In the 2020 NBPP, HHS added a new subsection § 156.130, which reads as follows:

(h) Use of drug manufacturer coupons. …

(1) Notwithstanding any other provision of this section, and to the extent consistent with state law, amounts paid toward cost sharing using any form of direct support offered by drug manufacturers to enrollees to reduce or eliminate immediate out-of-pocket costs for specific prescription brand drugs that have an available and medically appropriate generic equivalent are not required to be counted toward the annual limitation on cost sharing (as defined in paragraph (a) of this section).

In the preamble to 2020 NBPP it states that when no generic equivalent is available or medically appropriate, amounts paid toward cost sharing using any form of direct support offered by drug manufacturers must be counted toward the annual limitation on cost sharing.

It appears that the HHS rule requires the following:

(1) If there is an available and appropriate generic equivalent and the person uses a coupon, the plan is not required to count the amount of the coupon towards the OOPM.

(2) If a generic equivalent is not available or is not medically appropriate, the plan is required to count the coupon towards the person’s OOPM.

The only caveat is for insured plans that are regulated by the state, if the state has passed a law on this issue. To date, three states have issued such rules — Virginia, West Virginia and Arizona. Arizona law requires inclusion only if a drug does not have a generic equivalent or the patient has obtained access to the drug through prior authorization, step therapy or the plan’s exceptions and appeals process (Arizona HB 2166). Virginia and West Virginia require that all coupons count, no matter the circumstances (Virginia HB 2515; W. Virginia HB 2270).

Delayed Effective Date

On August 26, 2019, the IRS, DOL and HHS (the “Departments”) issued a joint FAQ (FAQ About ACA Implementation Part 40) addressing the 2020 NBPP. That FAQ stated the Departments had received feedback that GHP plan sponsors were confused about whether the 2020 NBPP required GHPs to count the value of drug manufacturers’ coupons toward the OOPM and how this worked with HSAs/HDHPs. In light of this confusion, HHS will clarify the application of the rule in its 2021 NBPP, and the Departments will not initiate an enforcement action if a GHP excludes the value of drug manufacturers’ coupons from the OOPM, including circumstances in which there is no medically appropriate generic equivalent available. However, this would not overrule any similar State Insurance law that has already passed. (State insurance laws are not applicable to self-funded ERISA GHPs.)

What Was HHS Trying to Fix?

It appears one reason that HHS issued this rule could be the lack of generic drugs on PBM formularies. Coupons are often used for expensive brand drugs.

A PBM formulary may not include a generic drug because the PBM would rather include a brand drug on the formulary that pays a large rebate (and other indirect compensation) to the PBM. (Those monetary benefits received by the PBM related to those brand drugs often will not 100% pass through to the GHP.) This HHS rule appears to encourage the addition of generic drugs on the formulary by allowing the GHP to ignore the coupon for purposes of the OOPM. Ignoring the coupon would cause participants to remain subject to the deductible for a longer period of time. This potentially could cause some participants to push for more lower cost generics to be included on the formulary.